Many myths regarding reverse mortgage loans circulate and can steer homeowners away from a great loan option. Unlike typical home loans, reverse mortgages allow you to convert part of your home equity to cash, as long as you are 62 or older. If you want to supplement your retirement funds, a reverse mortgage can be helpful. Additionally, you can use a reverse mortgage to pay off an existing mortgage or credit card debt.

At Senior Lending Corporation, we care about your retirement and finances, which is why we don’t want you to ignore this option because of misleading information. Below are some reverse mortgage myths we’re happy to debunk.

Due to this myth, many homeowners believe the dangers of reverse mortgages include owing more on your home than it’s worth. The truth is that you don’t owe more on your home than its value when sold when you have a Home Equity Conversion Mortgage (HECM).

Fact: Reverse mortgages are backed by federal insurance, and you are protected if your loan balance exceeds your home’s value. As a non-recourse loan, a reverse mortgage ensures you won’t be liable for more than the value of your home.

One of the perceived negatives of reverse mortgages stems from the myth that the lender will take ownership of your home when you get a reverse mortgage. We’re happy to report this myth is not at all true.

Fact: When you borrow a reverse mortgage, you keep the title and ownership of your home. As long as your home is your primary residence and you keep paying your home insurance and property taxes, you’ll retain ownership of the home.

In rare events, the home could go into foreclosure if a borrower doesn’t comply with their loan terms. Of course, this applies to just about any standard home loan and is not unique to reverse mortgages.

Fact: If you choose to borrow a reverse mortgage, your Social Security, pension and Medicare benefits will not be affected. However, some benefits could be affected, such as your Supplemental Security Income (SSI). If you are concerned about your benefits, discuss your situation with us at Senior Lending Corporation.

Medicaid is a bit different since it’s a need-based program. Your Medicaid benefits could potentially be affected by a reverse mortgage, so you may want to consult with a financial advisor to discuss your circumstances and determine what might be the best option for you.

Read our comprehensive reverse mortgage guide!

Fact: Your heirs can choose to sell your home to repay the mortgage if you haven’t paid it in full yet. In this case, your children will inherit the equity that remains in your home after your loan is paid off. Since many homes appreciate over time, heirs usually retain equity. Alternatively, your children can decide to keep your property as their inheritance and find another way to repay the loan, such as through refinancing. Regardless, your children won’t lose their inheritance if you choose a reverse mortgage.

A similar myth is that your children will be responsible for repaying your reverse mortgage. Luckily, since this is a non-recourse loan, the lender is repaid only from the proceeds of the sale, and your remaining proceeds will go to your children. The obligation of your outstanding reverse mortgage is attached to your property rather than your estate.

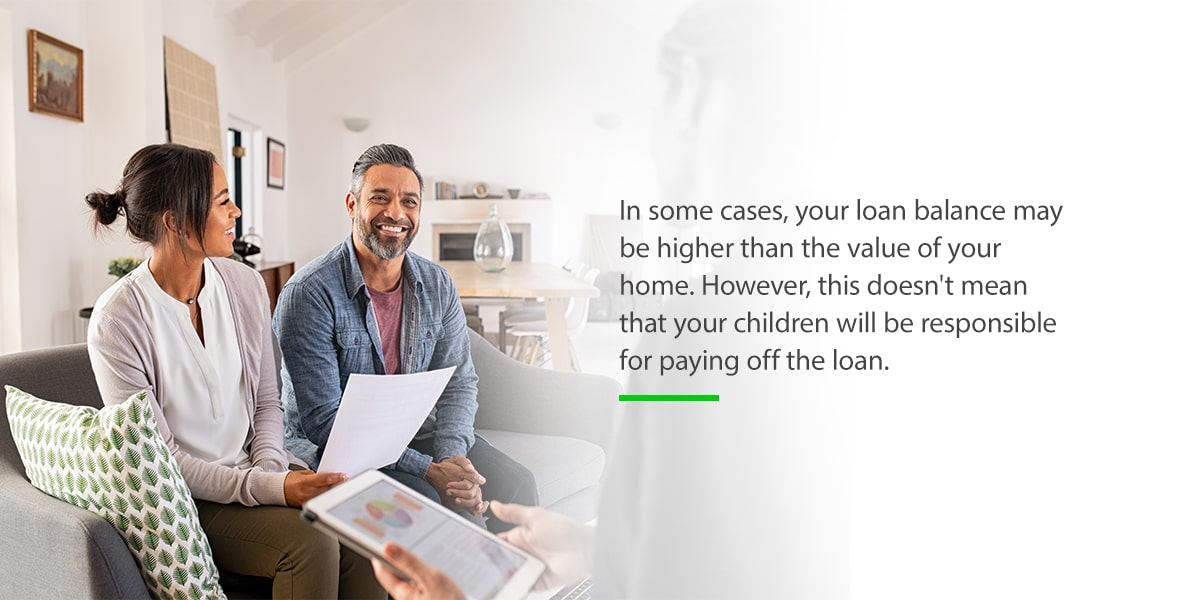

Fact: In some cases, your loan balance may be higher than the value of your home. However, this doesn’t mean that your children will be responsible for paying off the loan. In this case, they won’t be financially liable for the difference.

Fact: With a reverse mortgage, you don’t need to make a monthly mortgage payment if you continue meeting your loan terms. This means you should continue paying your home insurance, property taxes and HOA dues while maintaining your home.

You can opt to make payments that reduce your loan balance if you want, but the loan isn’t due unless you don’t meet your loan terms or until the last borrower leaves the home.

Fact: A reverse mortgage is similar to other types of home loans. If you sell your house, your reverse mortgage will be repaid when you close. If you want to sell your home in advance or make early payments, there aren’t any prepayment penalties.

Fact: A common myth around reverse mortgages is that you need excellent credit to qualify. Though your lender considers your income and credit to ensure you are in a stable financial situation and can afford your insurance, taxes and maintenance, your reverse mortgage requirements aren’t as stringent as a traditional mortgage.

So don’t disqualify yourself from a reverse mortgage based on your credit, and speak with a reverse mortgage company first!

One of the myths homeowners hear most often is that reverse mortgage borrowers often default on their loan or get foreclosed on.

While this may have been true for some borrowers previously, today’s rules and processes help many borrowers avoid this situation. Lenders complete financial assessments that make sure borrowers can meet their financial obligations.

Fact: In the cases where borrowers can’t meet their financial obligations, money from the loan proceeds could be set aside to pay insurance and taxes so borrowers can meet their loan terms. Today, foreclosures and defaults for reverse mortgages are low.

The myth that you can’t get a reverse mortgage because you already have a mortgage keeps many homeowners from applying.

Fact: The truth is that you can use your reverse mortgage to repay your existing mortgage and eliminate your monthly mortgage payment. Remember that you’re still responsible for remaining current on your insurance and taxes.

These myths can lead homeowners to believe that the pitfalls of reverse mortgages make these loans a poor choice. At Senior Lending Corporation, we hope that by debunking these myths and sharing the truth about reverse mortgages, you can rest assured that a reverse mortgage may be a good choice for you.

As a reverse mortgage company, we can help you make the best decisions for your retirement. When you choose Senior Lending Corporation, you’ll get a team you can depend on that understands your needs. Call us at 800-822-1190 for more info on reverse mortgages, or fill out our contact form.