When you have bad credit, it’s easy to think you won’t qualify for any loans or financial assistance without improving your score. With bad credit, you need financial help to get you out of your situation.

While poor credit history can limit your options, if you’re a senior homeowner, you’ve got a great option at your disposal — a reverse mortgage home equity conversion loan (HECM). A HECM differs from a regular mortgage in that you receive payments via your home equity rather than making payments toward a mortgage.

The good news is that the HECM is NOT based on any certain credit scores. In fact, having NO credit score is okay. Since you’ll be getting paid rather than the other way around, your credit score is not the best indicator of whether this option is right for you.

Jump To What You’re Looking For Here:

There are three stipulations to qualify for a HECM, which make up about 95% of the reverse mortgage market:

You’ll be happy to note that none of these qualifications rely on your credit score.

There are a few other disqualifiers, like outstanding federal debt, but generally, there are no credit score requirements in the approval process for a home equity loan.

Read our complete guide on reverse mortgages

Bad credit aside, there are a number of other things you should consider before applying for a reverse mortgage:

Although we’ve discussed how you can qualify for a home equity loan with bad credit, you may be wondering if there’s an exact threshold for your credit score to be approved.

There is no set minimum credit score that can tell you if applying for a reverse mortgage is worth your time. However, this can also be a benefit, as it means that no one is denied right away solely based on a number.

Also, remember that for reverse mortgages, bad credit doesn’t matter in the same way as it would in other lending situations. With these mortgages, you receive money, and the funds will only need to be paid back if you sell the home. As long as you can prove you can manage your home-related payments, your exact credit score is unimportant.

View Frequently Asked Questions

Since you aren’t necessarily making monthly payments for a reverse mortgage, it’s unlikely the loan will be a detriment to your credit score.

Still, that’s not to say there’s no credit check at all for a reverse mortgage. When applying for your reverse mortgage, a provider will complete a credit check as part of their financial assessment. The financial assessment checks for any barriers in your payment history that might affect your ability to keep up with your end of the loan. However, the provider likely will not report the loan to credit agencies.

In the case of reverse mortgages, a financial assessment looks at things more important than your credit score, including:

These indicators speak clearly to whether you’re able to maintain the guidelines of your reverse mortgage. If you have any of these blemishes on your report — even if they happened years ago — be prepared to explain the circumstances in detail and how you plan to uphold these criteria in the future.

In short, yes, you can get a reverse mortgage if you owe taxes, but in most situations, you need to do a bit of work before you receive approval.

If you owe federal or state taxes, the best solution is to resolve these concerns before moving forward with the reverse mortgage application. When you’re behind on tax payments, it’s likely you’re dealing with a bad credit score, which affects providers’ willingness to work with you. If you choose to move forward with your application, you may need to complete a few extra steps to get everything in order.

First, you’ll need to talk with the IRS. Based on your situation, the IRS may have already placed a tax lien on your credit, which makes them entitled to your taxes or other personal property until you make a repayment plan. If you own a home, this lien often diminishes your house’s equity. When you talk to the IRS, you’ll come up with a repayment plan together so you can get out of tax lien status and keep your account up to date.

Now, you can start making new payments on your taxes. In most cases, providers will require proof of your repayment plan, proof of adequate income to cover the payments and at least three months of on-time payments to justify the risk of working with someone who owes taxes.

A benefit of a reverse mortgage is that any tax liens can be paid off with the proceeds from your HECM at closing. So, tax liens will not keep you from qualifying for a reverse mortgage.

Factors like credit card debt or federal student loans don’t necessarily disqualify you from receiving a reverse mortgage. While you can still acquire the loan, you must pay off these debts with the money you receive before using the funds for other purposes.

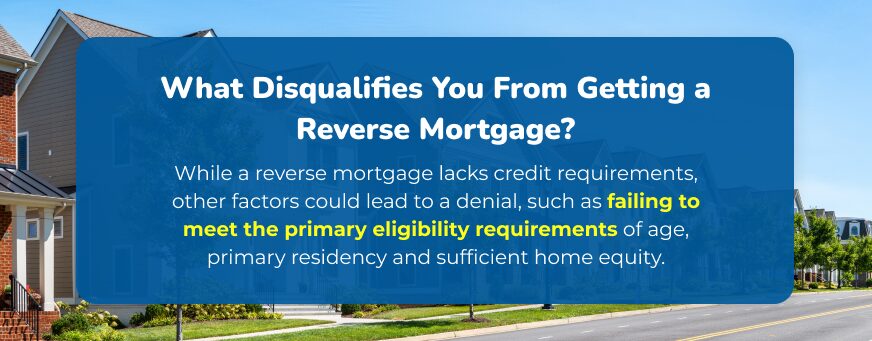

While a reverse mortgage lacks credit requirements, other factors could lead to a denial, such as failing to meet the primary eligibility requirements of age, primary residency and sufficient home equity. For example, applying for this lending option on a vacation home could result in a denial.

Other situations that could lead to disqualification include insufficient income to pay property taxes and homeowners insurance. Since counseling is a requirement for a home equity conversion mortgage, you will receive a denial for not completing a counseling session.

Reverse mortgages have no specific income requirements to qualify. The provider will analyze your finances to ensure you can pay property taxes and homeowners insurance and maintain the home. Even in cases with limited income, providers may allow for extenuating circumstances, such as Supplemental Security Income (SSI) benefits.

We’re committed to helping you achieve your retirement goals through trusted advice and federally insured lending options. Our team includes experts with years of experience helping seniors gain reverse mortgages. We walk with you through every step, including discussing eligibility requirements so you can confirm whether a HECM is the right choice for you. Seniors who have worked with us have seen how we build relationships and offer professional advice during the lending process.

Our organization carries licensing from the Nationwide Mortgage Licensing System, meaning we are qualified in our jurisdiction to provide mortgage options. This qualification also signifies that we stay current with all licensing requirements, including continuing education.

In many cases, taking out a reverse mortgage is simply a smart money move. You don’t need great credit to get one, and the money you receive from it can actually help you improve your credit over time.

Your retirement funds are too important for you to let them fall into the wrong hands, so you must choose a trusted company that works closely with you to help you understand everything.

If you’re unsure about whether a HECM loan is the best option for you, seek out expert guidance.

Senior Lending Corporation’s team of licensed advisors are people you can count on to help you achieve your goals and get some peace of mind about your finances. Give our advisors a call today at 800-822-1190 or reach out online to learn more about your options and get started with your reverse mortgage.