Many older adults wish to supplement their income before and during retirement. A reverse mortgage loan allows you to use your home’s equity and convert it into retirement income. The first reverse mortgage was issued in 1961, but reverse mortgages have received many enhancements and improvements in the past 10 years. They help older adults retire in their homes and enjoy added financial freedom once they reach the reverse mortgage age.

At what age can you do a reverse mortgage? Age plays an essential role when exploring these financial opportunities, and this guide walks you through the current reverse mortgage age requirements, including updates for 2025.

A reverse mortgage allows you to borrow from your home’s equity, using it to fund an income stream for your retirement. A reverse mortgage is a loan you receive all at once or arrange monthly payments. You can even use it as a line of credit.

This loan is different from a traditional mortgage, where you receive funds and repay the loan via monthly payments. Instead, a reverse mortgage pays you, and you repay the loan when you move out, or it gets repaid when you pass away. In return for these funds, the lender charges interest and fees, deducted from the home equity.

Reverse mortgages can provide many benefits for older adults. For example, you can use the money to cover unexpected expenses, pay bills, make home repairs or enjoy a well-earned vacation.

Once you’ve qualified for a reverse mortgage, you can use the money however you want — meet daily living expenses, cover medical bills or pay off debt. The reverse mortgage company pays you, the homeowner. You remain responsible for fees and home maintenance and don’t have to make any payments against the balance until you cease using the home as your principal residence. There are two main types of reverse mortgages as follows:

Learn the Reverse Mortgage Basics

Yes. Age sets the foundation for eligibility, but the age requirement for a reverse mortgage depends on the mortgage you are applying for. The federally insured Home Equity Conversion Mortgage requires at least one borrower to be 62. Proprietary reverse mortgages offer a different path, giving homeowners access as early as 55. Understanding at what age you can do a reverse mortgage helps you choose the option that matches your plans and timing.

An HECM can provide more flexibility than a traditional home equity line of credit since you can draw funds as needed without being required to make monthly payments. Many retirees appreciate the structure and long-term flexibility it offers. Because you continue to own your home, you stay in control of your property while accessing a portion of its equity without taking on monthly payments. These funds may help cover essentials such as home insurance, taxes or repairs, along with groceries or personal expenses that soften your monthly budget.

HECM age requirement:

• 62 or older

• Sufficient equity

• Occupy the home as your primary residence

For homeowners who want earlier access, proprietary products expand the possibilities. These are privately offered programs that allow access at age 55.

Proprietary reverse mortgage programs are available for homeowners between 55 and 62 whose homes’ values exceed the HECM limit. These programs are also called jumbo because homeowners can access larger amounts than HECMs.

At Senior Lending Corporation, we offer the HomeSafe Jumbo Credit Line, which allows borrowers to obtain a reverse mortgage of up to $4 million at age 55. The product enables you to make flexible payments, doesn’t charge prepayment or maturity date penalties, and the limit rises automatically each year for the first seven years.

Just like the FHA HECM, the HomeSafe Credit Line is non-recourse. However, since it is privately backed, it does have other criteria that must be met.

Contact Senior Lending to learn more about this reverse mortgage solution.

• Allows earlier access starting at 55

• Can be a match for higher-value properties

• Offers flexible payout structures

• Can support goals such as home improvements, lifestyle expenses or long-term planning

Many retirees explore the HomeSafe Credit Line, a proprietary solution designed to give you control over how and when you use your available funds. It works well for homeowners who want to prepare for unexpected costs or who prefer a line of credit structure instead of a lump sum.

No. There isn’t a maximum age for a reverse mortgage. You could qualify for a higher HECM loan amount as you get older.

| Feature | HECM (62+) | Proprietary (55+) |

|---|---|---|

| Minimum Age | 62 | 55 |

| Federally Insured | Yes | No |

| Ideal For | Broad retirement planning | Higher-value homes or early access |

| Counseling Required | Yes | Yes |

| Primary Residence | Required | Required |

| Sufficient Equity | Required | Required |

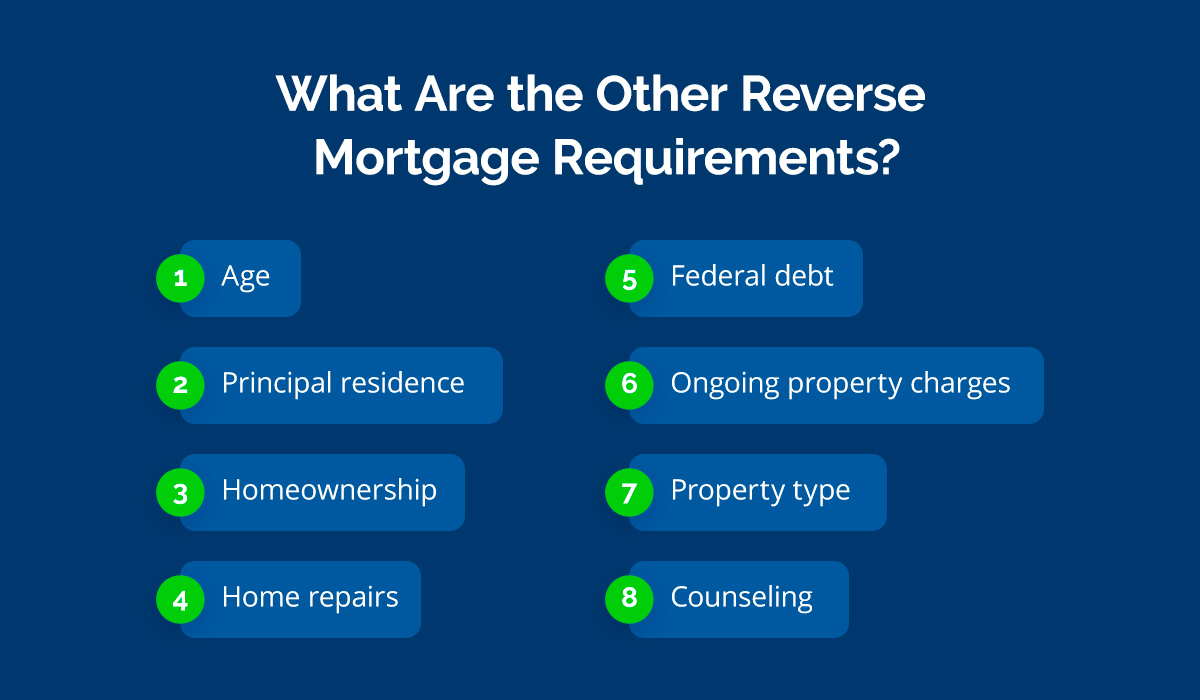

What age qualifies for a reverse mortgage isn’t the only factor to consider when applying. For a HECM reverse mortgage, you are required to meet the following criteria:

The requirements for a proprietary reverse mortgage are similar except for the age, term flexibility and federal insurance exceptions. Because proprietary reverse mortgages are not federally insured, most options do not require up-front mortgage insurance or monthly premiums. Proprietary programs can approve property types on and off the FHA list, like warrantable condos.

Keep in mind there are also costs associated with a reverse mortgage, such as origination fees, closing costs, interest and loan-servicing fees.

Feel confident in funding your retirement with our reverse mortgage products because we care about helping you fulfill your financial goals. Through a supportive and empowering approach, combined with years of experience, we provide relationship-driven solutions that make a difference.

We’ll assign you a dedicated licensed advisor to guide, support and meet your needs. They’ll prioritize understanding what you want and delivering it effectively and honestly.

Past clients have had such rewarding experiences with their advisors that they recommend us to anyone looking for retirement funding. They have written raving reviews appreciating our advisors’ professionalism, friendliness, efficiency, timeliness, expertise, commitment, assistance and patience. One client was considerably impressed when their advisor continued answering his questions post-closing.

A reverse mortgage can be life-changing for you and your family. Senior Lending Corporation can provide you with the trusted financial opportunity of a lifetime and help you make your retirement dreams a reality. If you’re interested in exploring the exciting possibilities of a reverse mortgage, we can help.

We’re a team of licensed advisors passionate about providing our customers with the best possible experience. We understand your needs and will work together with you so you can live your retirement your way.

Dial 800-822-1190 if you’d like to speak to a reverse mortgage expert to learn how the HECM and proprietary programs work. Alternatively, please get in touch with us online, and one of our licensed professionals will get back to you and talk you through this fantastic opportunity.