Older adults sometimes need additional funding to support their retirement. The challenge is that most lending arrangements demand high credit scores and other complex requirements, making them inaccessible to many.

With a reverse mortgage, you can receive money as a monthly payment, as a line of credit or in lump sums. This arrangement allows to pay off high interest credit cards, make needed home repairs or improvements, pay off existing mortgages to increase cash flow or for any purpose.

This article will help you understand reverse mortgage basics and what it takes to get your loan approved.

A Federally Insured reverse mortgage (HECM) allows homeowners to borrow money using their homes as security. However, the borrower does not have to make monthly mortgage payments, unlike with traditional mortgages. Instead, the borrower receives payments from the lender — hence the term “reverse.” The borrower repays the loan amount when they no longer live in the home, like when they move out permanently, sell the property or die. It’s a unique and beneficial lending transaction.

Federal regulations require lenders to structure the loan amount to stay within the home’s value. Additionally, reverse mortgage applicants may still get loans despite having low credit. Homeowners who get reverse mortgages borrow against the value of their homes and receive funds as monthly payments, as a line of credit or in a lump sum. You can spend this money however you like, such as to cover utilities and other bills, buy groceries or go on vacations.

An eligible person can apply for a reverse mortgage in Texas using their home’s equity. Your home’s equity is the actual value of your property, which is your home’s current market value minus any outstanding loans or liens.

Applying for a reverse mortgage in Texas is a streamlined process. There are minimal income and credit requirements and the entire process from start to finish can be completed within 30 days.

The borrower is required to pay property taxes and homeowners insurance and use the property as their primary residence. The borrower continues to hold the title to the home.

There are two types of reverse mortgages — home equity conversion mortgages (HECM) and proprietary reverse mortgages.

A HECM which is Federally Insured is the most common type of reverse mortgage. It’s specially designed to help retirement-age homeowners gain better control over their mortgage repayment obligations.

With a HECM, the borrower can withdraw a portion of their home equity to supplement their retirement funds. The lender then provides tax-free funds without requiring monthly payments from the borrower.

The Federal Housing Administration (FHA) insures the loan and regulates the fees. Typically, there are minimal income requirements.

The program allows you to retain full ownership of your property and offers added benefits, including the following:

Flexible payments: A HECM lets you pay any amount at any time toward your balance. For example, you can pay the principal only and interest later or make zero payments. This setup helps retirees live comfortably without worrying about repayment notices.

Flexible payments: A HECM lets you pay any amount at any time toward your balance. For example, you can pay the principal only and interest later or make zero payments. This setup helps retirees live comfortably without worrying about repayment notices.Unlike the FHA-insured HECMs, proprietary reverse mortgages are backed by private lenders. They’re ideal for those with homes appraised at high values. Typically, you qualify for a proprietary reverse mortgage if your home is worth more than the federal HECM lending limit. Homeowners with less mortgage balance may be eligible for more funds and receive the money as a line of credit or a single lump sum payment.

Because proprietary reverse mortgages are privately backed, the federal government does not underwrite or insure the loan. Also, the loan’s terms may not comply with the FHA limits. These loans have higher interest rates and may attract added fees. However, they offer more funds and flexibility — in some cases, borrowers as young as 55 can qualify.

Here are the requirements to qualify for a HECM:

Other reverse mortgage qualifications may include:

A typical reverse mortgage process involves the following steps:

Once you find a reliable institution, fill out and submit the application for the reverse mortgage. Depending on the company, you can apply online or in person.

The lender will usually share a standard estimate and provide other relevant information, such as the interest rate and fees. You will also discuss the loan amount and method of payment, whether as a lump sum, a line of credit or a monthly payment. Terms will only be approved after the lender understands your financial situation and the equity remaining in your property.

The lender will ask you to provide documentation so they can verify your identity and conduct a background check and determine that you qualify for the loan. The required documentation usually includes the following:

It’s essential to gather the necessary documents before applying for a loan to avoid delays. You may contact the lender to ask what information they need from you before taking any steps.

The FHA rules require every reverse mortgage borrower to undergo counseling with an approved professional. This process is meant to educate the borrower on the benefits and potential challenges associated with the loan transaction. If there are alternative means of funding, the counselor may guide the borrower through those avenues. You can search for a counseling agency on the FHA portal, which provides a list depending on your location.

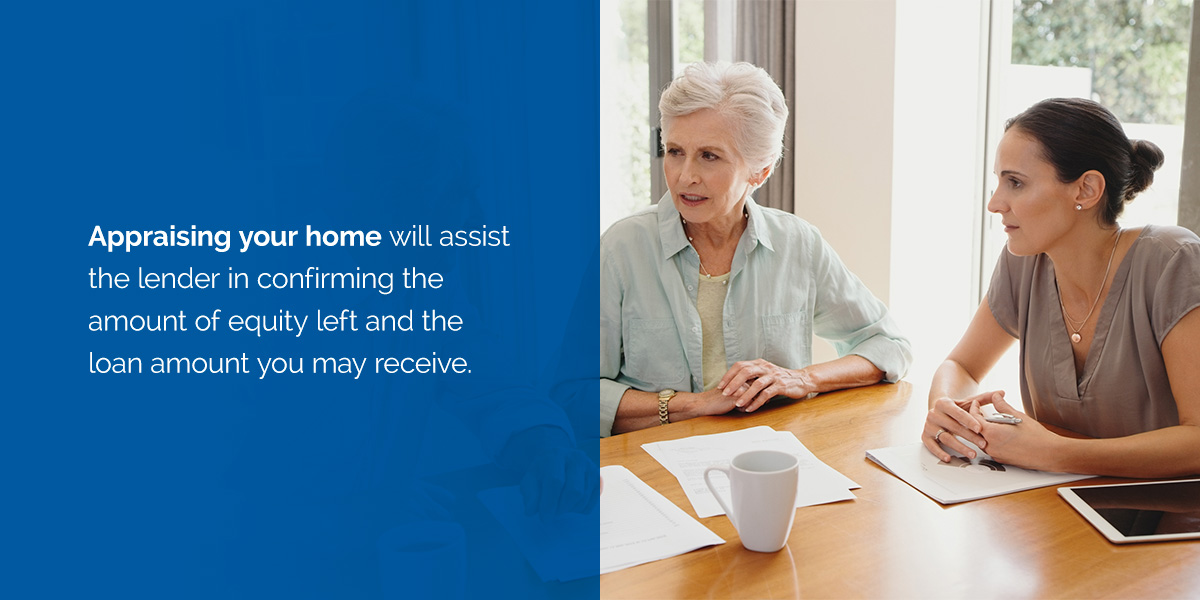

The lending company will appraise your property to know its market value. Appraising your home will assist the lender in confirming the amount of equity left and the loan amount you may receive. Remember, the FHA sets annual limits, and your home’s value can determine how much money you get. The FHA must approve the appraisal before the lender can proceed.

A title search is usually conducted to confirm ownership of the property. If there are prior or conflicting owners or lapses in ownership, additional paperwork may be required to clear the title. After verifying the home’s ownership, the underwriter may review the appraisal financial assessment and ensure compliance with the guidelines.

At the final stage of the process, the lender will review all aspects of the loan and obtain the signatures on the loan documents with a notary. The lender will then pay the money to the borrower in the manner agreed between the parties. You can then use the funds however you please.

HECMs offer older adults many advantages, including the following:

A reverse mortgage allows you to continue living in your home as long as you want while getting money from the lender. There is no requirement to find alternate accommodation or transfer the title to the lender. This kind of arrangement is most suitable for older adults who want to raise funds to supplement their retirement income without selling their properties.

The federal government insures the reverse mortgage loan, providing you with a higher level of security. If the loan amount exceeds the home’s value, the government will cover the difference.

A HECM reverse mortgage is a non-recourse loan, meaning the lender may not go beyond the security — in this case, the home. By extension, your children or heirs are also protected when they inherit the property.

Some revenue generation alternatives attract high tax rates, but that is not the case for reverse mortgages. Even as you continue to pay property taxes and other expenses like insurance, the proceeds from the reverse mortgage are exempt from taxes.

Unlike other loan arrangements, reverse mortgages let you receive money without making monthly payments as you continue to live in the property. Again, unlike traditional mortgages, reverse mortgages do not attract penalties.

Reverse mortgages provide borrowers with flexible payment options according to their needs. You can use the money to fund any of your expenses — there are no limitations on how you can spend the money.

Yes, you can sell a property with a reverse mortgage. Selling the property lets you pay off the loan and other related expenses and keep the rest. There are no penalties. However, it’s best to consult your loan servicer and get a payoff quote in writing before selling your home.

The homeowner owns the home in a reverse mortgage not the lender. The home is only used as security for the loan just like with a traditional mortgage. Note that the agreement may require you to meet requirements like keeping your house in good condition and paying property taxes and homeowners insurance, which you likely already do.

The properties that qualify for FHA-insured loans like HECM loans include:

Newly constructed homes are eligible for HECM loans if the local authorities issue a certificate of occupancy or its equivalent.

While HECM loans are designed to assist as many retirees as possible, some properties may not qualify. Here are some examples:

Reverse mortgages have no set payment times. They are triggered when one of the following happens:

Other repayment options include refinancing the mortgage, which means you can take out a new mortgage to pay off the reverse mortgage or just sell the home.

Senior Lending Corporation helps older adult homeowners in Texas get the funding to support their retirement. Our trained HECM specialists will listen to your concerns and provide practical and flexible solutions according to your needs. You can trust us to match you with the right program.

If you’re located in Texas and want to learn more about reverse mortgages, you can contact us online today or call a licensed advisor at 800-822-1190.