Planning for long-term care, whether for yourself or a loved one, can be challenging when it comes to finances. Reverse mortgages can be a good option to help pay for long-term care as they help to increase your income so you can pay for additional expenses. These expenses can include making your home more accessible, moving your non-borrowing spouse into an assisted living facility or paying off debts. While insurance premiums are often the majority of health care expenses, retirees will likely still spend thousands out of pocket during the rest of their life.

Before you convert a portion of your home equity into loan proceeds, ensure that you fully understand the mechanics of this loan.

You can take out a reverse mortgage by borrowing from your home equity, which is the difference between the property’s value and the total amount owed on any outstanding mortgage loan. For example, if the home is appraised at $500,000 and the mortgage balance amounts to $200,000, the home equity sits at $300,000. These loans are available to homeowners 62 and older to help them stay in their homes for longer.

You should consider two types of reverse mortgages — Home Equity Conversion Mortgages (HECMs) and proprietary. Eligibility for either option depends on your payment history and whether you have significant equity in your home. On approval, you can elect to receive funds as a lump sum, monthly payments or a line of credit:

Repayment only starts with triggering a “maturity event” like the home sale. This trigger includes circumstances like if the borrower cannot keep up with property expenses or if the borrower moves out of the house.

An HECM is a popular option for single-family homes, condominiums, townhouses, multiple-unit homes and manufactured houses. The Federal Housing Association (FHA) insures these loans. The FHA lending limit on this reverse mortgage in low-cost areas is $498,257 and $1,149,825 in high-cost areas.

When you receive funds from this loan, you must first repay the money you borrowed against the home. Then, you can use your funds to pay for a nursing home or other long-term care option that suits your needs. Additionally, you can allocate funds towards out-of-pocket medical expenses or home-safety modifications.

Proprietary reverse mortgages are private loans that cater to homeowners with high-value properties. This characteristic gives them their other name — jumbo reverse mortgages.

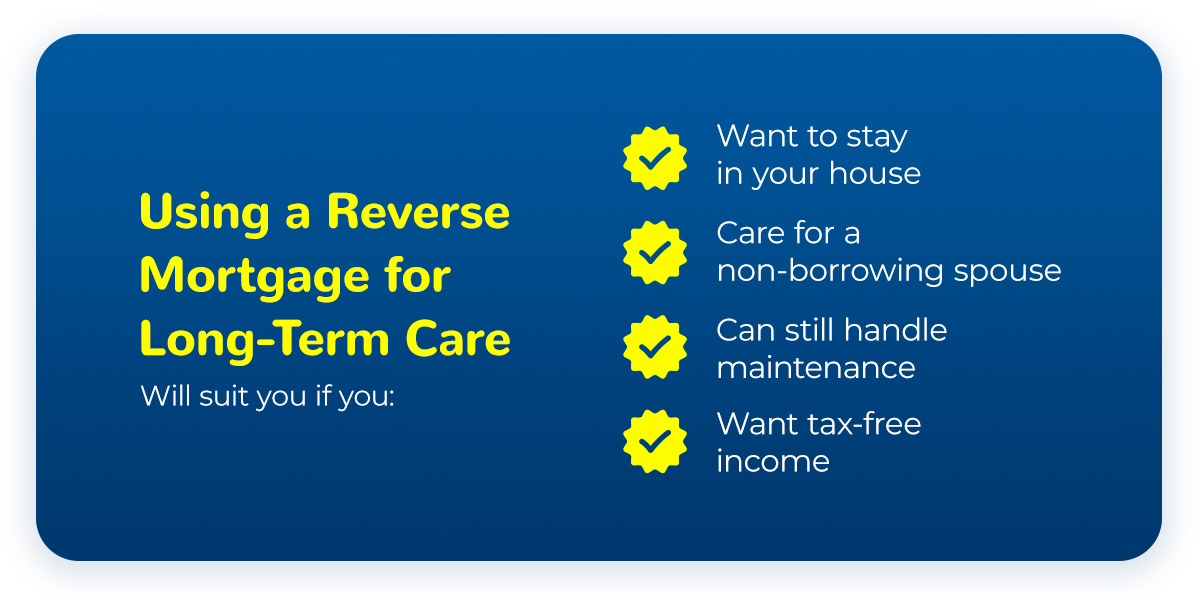

Traditionally, people use a combination of personal savings, insurance policies, Medicaid, pensions and retirement accounts to fund long-term care. Sometimes, family support, annuities or investment income also help cover costs. Veterans and their spouses may use Veterans Affairs (VA) benefits. If you opt for a HECM, you can choose between fixed and adjustable rates. Using a reverse mortgage for a nursing home or other long-term care will suit you if you:

One of the most significant benefits of a reverse mortgage is that payments are not taxable. They will not affect your Social Security or Medicare benefits. They also offer you financial flexibility and security, allowing you to use your reverse mortgage for assisted living or any other form of long-term care you need.

Reverse mortgages come with some upfront and ongoing costs like the origination fee, closing costs, counseling service costs, interest, loan-servicing fees and the FHA mortgage insurance premiums. Also, check that your reverse mortgage has a “non-recourse” clause, which ensures that neither you nor your beneficiaries will owe more than the home is worth.

Ideally, you want to cover your expenses without alternative funding sources. So, determine how much you need to fund your long-term care or the changes you need to make to your home. The funds you can get from a reverse mortgage loan must be enough to cover these expenses.

Consider what, if any, impact the future sale of your home might have on your finances and estate planning. For example, if you plan to sell your home, ensure you have enough equity for you or your beneficiaries after paying off the reverse mortgage loan.

While this loan option is relatively straightforward, consulting with a financial advisor is always best. There are many myths about HECMs, so ensure you understand how this will impact your finances before making a commitment. Some common FAQs about reverse mortgages include:

Taking on a reverse mortgage is a financial decision that can take off a significant amount of pressure if you need to plan for long-term care for yourself or your spouse. This care can extend to supporting in-home care, assisted living or nursing home costs.

Senior Lending Corporation can help you fund your retirement your way. We offer you flexible solutions and advice from licensed advisors who will be with you every step of the way. Call us today at 813-590-1749 for more information or complete our contact form, and we will confirm how much you qualify for on a reverse mortgage.