Over the years, you made mortgage payments to your lender, reducing the amount you owe and building equity in your home. You might now have a sizable nest egg, but it’s locked into your house. With reverse mortgage loan advances, you can access this equity and put it to use for your current financial needs.

A reverse mortgage loan lets you tap into your home’s equity, giving you the cash you need to pay for your living expenses or cover unexpected bills. The Federal Housing Administration (FHA) insures the Home Equity Conversion Mortgage (HECM). It’s the only federally-insured reverse mortgage program available.

A HECM reverse mortgage can help you reach your financial goals but might affect your eligibility for Medicaid and other types of government aid. Learn more about Medicaid eligibility and reverse mortgages and how they might affect you.

Quickly Jump To What You’re Looking For:

To qualify for a HECM Reverse Mortgage, you need to meet certain requirements. For Example at least one borrower must be 62 or older to qualify. FHA now allows the other spouse to be under 62 years of age. You also need to own your home and plan on continuing to live in it. In Florida, you need to attend a counseling session before getting a HECM.

Learn more about reverse mortgages

Medicaid is a public health insurance program for people who have low incomes. It’s not to be confused with Medicare, which is the federal health insurance program primarily for people over the age of 65.

If you meet eligibility requirements, you can qualify for Medicaid at any age. About 20% of people in the U.S. qualify for Medicaid.

Medicaid is a federal program but is administered by individual states. That means the requirements might be slightly different from state to state. In Florida, a two-person household’s maximum income to qualify for Medicaid is $24,353.

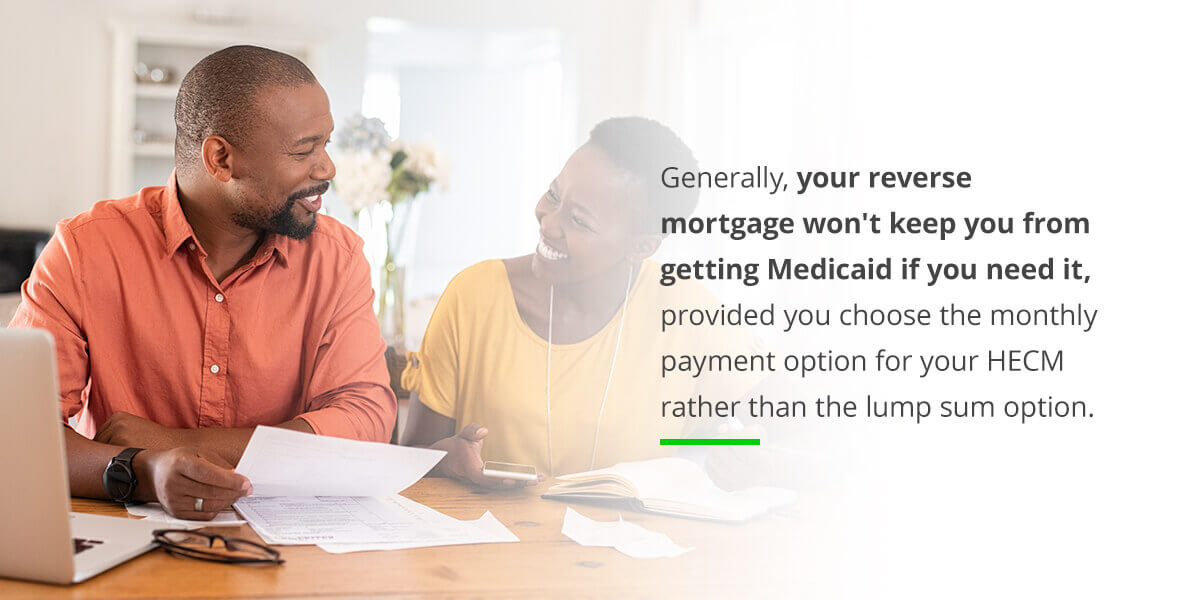

If you plan on getting a HECM, you might be concerned that a reverse mortgage will affect your Medicaid benefits, since the proceeds from the HECM can increase your monthly income. It’s important to understand how Medicaid rule insurance regulation might impact your benefits to ensure that your financial planning remains on track. Generally, your reverse mortgage won’t keep you from getting Medicaid if you need it, provided you choose the monthly payment option for your HECM rather than the lump sum option.

If you’re concerned that your HECM will affect your benefits, it’s a good idea to discuss it with a counselor before you apply for a reverse mortgage.

Medicaid is an example of a means-tested benefit. A means test examines your financial situation when determining whether you qualify for a program or not. In the case of Medicaid, the state will ask to see proof of your income and request information on your assets.

Medicaid recipients typically need to have an income below the federal poverty line. They also need to have a limited amount of money saved in the bank to qualify.

If you receive enough money from your HECM each month to save part of it, you might soon have enough assets to fail the means test and potentially lose your Medicaid benefits.

Depending on your financial circumstances, you or your spouse might also receive supplement security income (SSI) benefits from the government. SSI benefits aren’t the same as Social Security. They are paid for from general tax revenues.

The benefits are for people who are older, disabled or blind and who have almost no or no income.

If you want to receive SSI benefits, your resources need to be less than $2,000 if you’re single or $3,000 if you’re in a couple.

The program doesn’t count the home you live in as a resource, but it might count the income you receive from a reverse mortgage if you put that money in an account and start to save it.

Your eligibility for other government benefit programs can also be affected by a HECM. If you’re a veteran who can receive a veteran’s pension, your pension payments can be affected if your net worth increases.

If you’re concerned about the effect a HECM will have on your government benefits, discuss those concerns during your counseling session.

A reverse mortgage counselor can help you weigh the pros and cons of a HECM and evaluate if or how it will affect your benefit eligibility.

Your home needs to be your primary residence if you want to qualify for a reverse mortgage. If you move into a nursing home permanently, you’ll need to pay back the reverse mortgage proceeds. This means settling the amount borrowed through the reverse mortgage before you can fully transition.

A permanent move is longer than 12 months. If you are only in the nursing home for six months, then return to your primary residence, you won’t have to pay back the reverse mortgage right away.

You can continue to enjoy the benefits of your HECM if your spouse moves to a nursing home and you stay in the home, or the reverse. At least one person from a married couple needs to remain in the home.

If you need to or decide to move to a nursing home permanently, you can use the proceeds from the sale of your primary residence to pay off the HECM.

If you’re interested in a reverse mortgage but are concerned about the impact it will have on Medicaid or other government benefits you receive, talk to an expert at Senior Lending Corporation today.

Our mission is to help you gain financial peace of mind regarding retirement. Sign up to receive a free information kit, or call us today at 800-822-1190 to speak to one of our advisors.