A reverse mortgage gives homeowners aged 62 or older access to cash by converting a portion of their home equity. The interest rates on a reverse mortgage determine the overall cost, which includes various reverse mortgage costs. These rates vary depending on the specific reverse mortgage program, market conditions, and the type of interest rate chosen.

Understanding the nuances of these loans and their interest rates allows you to make an informed decision, including whether to choose a fixed or adjustable rate, and find the most suitable reverse mortgage that aligns with your circumstances and financial goals.

How Do Reverse Mortgage Rates Work?

A reverse mortgage offers you a tax-free loan without making monthly mortgage payments. The amount of money you can borrow is based on how much equity you have in your home. Then, the loan gets repaid when you sell the house or pass away. The balance you owe increases over time because interest accrues every month. As a qualifying applicant, you can choose from a few different payout options:

Single lump sum: With this option, you receive your loan balance in a single payout

Regular fixed payment: This option gives you regular income for a set number of years or as long as you live in the house.

Line of credit: With this option, you can access the loan amount as needed or combine it with a monthly cash advance, depending on the loan’s terms.

A few key factors that define a reverse mortgage are:

Homeownership: Homeowners retain ownership of their homes as long as they meet the loan requirements, like having paid off a substantial amount of their mortgage, using the property as their primary residence, remaining current on their property taxes and paying off their existing mortgage using the proceeds from their reverse mortgage.

Fund use: People often use the funds from a reverse mortgage to supplement their retirement income, make home improvements, enhance their quality of life or cover medical expenses.

Loan cost: These mortgages have upfront fees like traditional mortgages, home equity lines of credit (HELOCs) or home loans without requiring monthly mortgage insurance premiums.

FHA counseling: You must meet with a counselor approved by the Federal Housing Administration (FHA) to ensure you fully understand the process of your reverse mortgage and the terms of your loan.

Three different reverse mortgage types are available. The most common, a Home Equity Conversion Mortgage (HECM), is the only reverse mortgage insured by the U.S. federal government and is only available through an FHA-approved lender. Proprietary reverse mortgages are open to anyone with a high-value property. Since private lenders offer and insure proprietary reverse mortgages, they are not backed by the federal government.

The least common, single-purpose reverse mortgages, are similar in that they allow borrowers aged 62 or older to borrow against their home equity but can only fund a single, lender-approved purpose. These are only offered in some states and by some government agencies and nonprofits.

Consider your financial standing when deciding between these two reverse mortgage interest rate options. It’s best to consult with a reverse mortgage counselor as you explore your options to ensure you select an interest rate that suits your lifestyle.

Fixed Interest Rates

This interest rate is well-suited to homeowners who want to use all their reverse mortgage funds simultaneously. Fixed interest rates remain the same throughout your reverse mortgage. In a financial market where interest rates fluctuate or are about to increase, your monthly payments will stay the same, adding the benefit of predictability for budgeting purposes. Some pros and cons include:

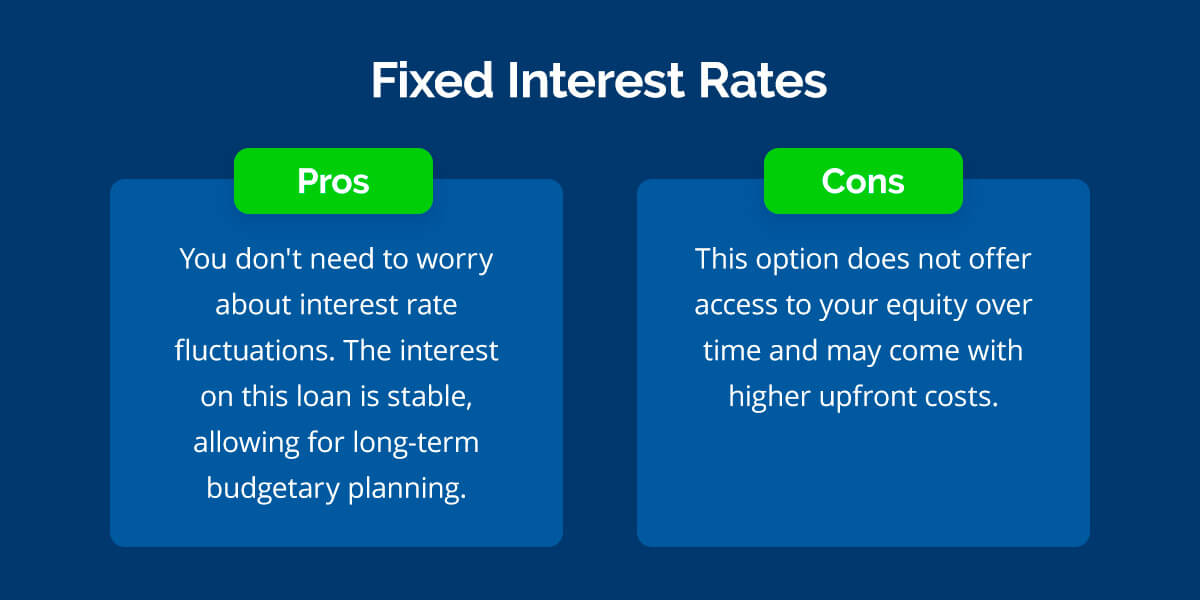

Pros: You don’t need to worry about interest rate fluctuations. The interest on this loan is stable, allowing for long-term budgetary planning.

Con: This option does not offer access to your equity over time and may come with higher upfront costs.

Variable Interest Rate

Also known as an adjustable rate reverse mortgage, this interest rate can change monthly or yearly due to its ties to financial indexes like the London Interbank Offered Rate (LIBOR) or Constant Maturity Treasury (CMT). You will often see a lower initial rate to appeal to homeowners.

All variable interest rate reverse mortgages have a lifetime cap, which is the maximum interest rate the loan can reach over its term. This cap protects against excessively high interest rates. As this interest rate changes, homeowners who want to access their equity gradually may decide on this option. Here are some pros and cons:

Pros: You have various options for accessing your home equity. This includes a line of credit, monthly payments or a combination. Variable interest rates can offer lower lifetime costs if interest rates remain stable or decrease over time.

Con: The interest rate can rise quickly and drastically based on the underlying benchmark rate despite staying within the lifetime cap.

How Often Does a Variable Rate Change?

The interest rate on a variable-rate mortgage changes monthly or annually, depending on the loan terms. If you have an adjustable-rate reverse mortgage, you may see interest rate changes that affect the overall cost and terms of the reverse mortgage. Additionally, the adjustment interval impacts how predictable your loan’s interest costs will be and how suitable the loan is for your financial circumstances. Three typical rate adjustment intervals may apply:

Monthly: The interest rate can change at the start of each new month, which can be advantageous if interest rates fall. However, this interval also increases the risk of rising costs with higher rates over time.

Annually: Alternatively, the interest rate may adjust once a year on the loan anniversary. This adjustment offers a balance between flexibility and stability, which is beneficial as it gives you some protection from rapid increases.

Other intervals: Loan providers may offer adjustable-rate HECM reverse mortgages with less common adjustment intervals, like quarterly or semi-annually. The terms and frequency of these rate adjustments can vary among credit providers and loan products.

Keeping an eye on your monthly mortgage statements helps you stay appraised on principal fees and interest accrued. It is worth noting that HECMs are non-recourse loans — the FHA guarantees that you or your heirs will never owe more than the home’s market value when sold to satisfy the loan balance. Your beneficiaries will not owe your credit provider more than said value when it’s time to repay the loan.

Are All Fixed-Rate Reverse Mortgages the Same?

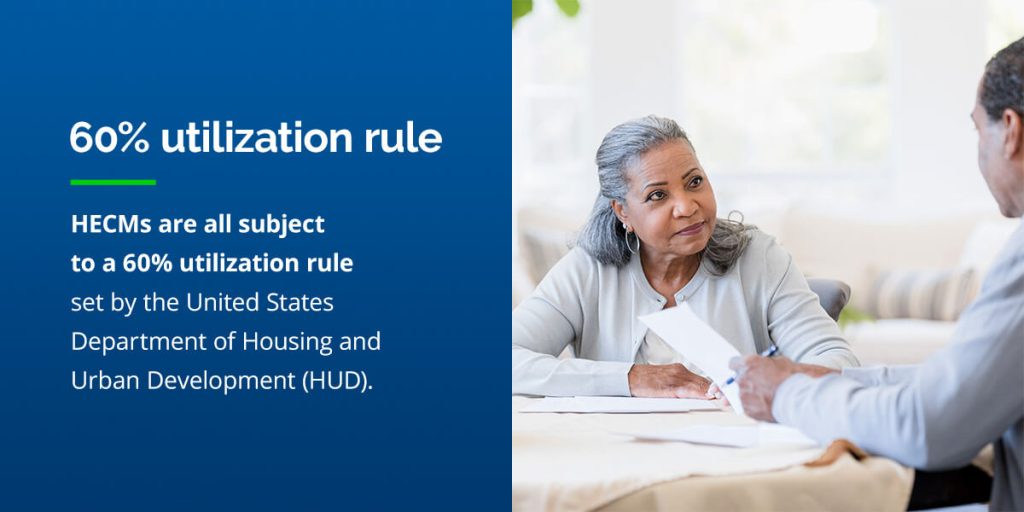

HECMs are all subject to a 60% utilization rule set by the United States Department of Housing and Urban Development (HUD). This rule places a cap of 60% on the amount of home equity you can take in the first year. This means homeowners have access to less equity than when they choose a variable interest rate. The exception to this rule is that you may pay off your existing mortgage and take an additional 10% of the available funds in your reverse mortgage loan.

Payment Plans Available on a Reverse Mortgage

Reverse mortgage payment plans are tailored to suit eligible homeowners’ various financial needs or preferences. Understanding the mortgage amount available to you can help in choosing the right plan. Six primary payment plans are available:

Lump sum plan: You receive one upfront payment.

Tenure plan: You receive monthly payments from your credit provider as long as you live in your home. The payment amount depends on factors like your age, home value and the current interest rate, offering you a stable source of income.

Line of credit plan: You can access funds up to the loan limit as needed. The portion of your unused line of credit will grow over time and may increase the equity you have access to.

Term plan: With this option, you receive monthly payments for a fixed term only — often five, 10 or 15 years. This option can help you meet specific financial goals like paying off debts.

Modified term plan: For a predetermined time, usually a few months, you receive a fixed monthly payment while having access to a line of credit. This is valid as long as the homeowner uses the property as their primary residence.

Modified tenure plan: You receive monthly payments and have access to a line of credit while you live in your home. The payments may be less than those available in a straight tenure plan but can still allow you to meet your essential monthly expenses.

Why Is a Line of Credit Not Available at a Fixed Interest Rate?

A line of credit offers flexible access to your equity. This loan type is not available with a fixed interest rate because of how reverse mortgage interest rates are structured:

Risk management: Fixed rates on a line of credit expose credit providers to the risk of rising interest rates, which can cost them more.

Higher costs: Homeowners can face less favorable options or terms due to increased expenses associated with their home equities, as credit providers need to balance their return on investment.

Less flexibility: Credit providers may need more flexibility to adapt to changing market conditions or interest rate fluctuations and lose this flexibility if locked into a fixed interest rate on a line of credit.

Less competitive marketplace: Variable-rate lines of credit can provide homeowners with more options as they can enjoy the potential for lower initial interest rates and flexible features to their line of credit payment plan.

Other Interest Rate Terms

As interest and additional fees accrue on your loan balance, understanding the interest rate environment can help you calculate where your loan stands. Different types of interest rates can affect the overall cost of your loan and provide insights into your financial situation.

Initial interest rate (IIR): This note rate applies to variable-rate loans. Interest throughout the loan’s life span is calculated using an IIR. This is the homeowner’s interest rate for the first month or year of the loan and is only in effect for the first LIBOR index rate period.

Expected interest rate (EIR): This rate applies to both fixed and variable rates and estimates the lifetime average rate of the loan. On a variable-rate loan, the EIR is based on a 10-year index. On a fixed-rate program like HECM, it is the same as the IIR and remains the same over the loan term. Essentially, this predicts rates to expect over the loan’s life.

The interest rates on reverse mortgages are based on factors like your age, the reverse mortgage loan rates, type of loan and your home’s value. Interest rates affect the amount of equity you can receive from your property. Interest rates can also affect:

Cost: The interest rate determines the overall cost of a reverse mortgage loan, which may or may not work in your favor.

Monthly payments: Variable-rate reverse mortgages may see lower rates that result in smaller payment amounts if the interest rate spikes or drops suddenly.

Loan balance growth: Interest accrues over time, which can impact how quickly your loan balance grows in an unfavorable market.

Repayment savings: When you repay your reverse mortgage through a home sale, lower interest rates give you a smaller loan balance, leaving you with more of the proceeds.

Line of credit growth: If you have this option with your variable rate, the interest will affect how your unused portion grows over time.

What Will Your Interest Rate Be?

Understanding the interest rates associated with a reverse mortgage is crucial as you explore your financial options. Whether you choose a fixed-rate or variable-rate, interest rates have benefits, costs and long-term implications on your loan. Working with a licensed advisor can help you make informed decisions.

Senior Lending Corporation offers reverse mortgage options that suit your retirement needs. Our dependable team provides comprehensive mortgage advice and compassionate services to help you run your retirement your way.